The Fed Prime Rate is one of the most important interest rates in the United States, and it affects millions of people every day. Even if you have never heard of it before, this rate plays a big role in how much you pay for credit cards, personal loans, and other types of borrowing. When the Fed Prime Rate changes, it can raise or lower the cost of borrowing money almost overnight. Because of this, understanding how it works can help you make smarter financial choices and avoid paying more than you need to.

For borrowers, the Fed Prime Rate acts like a base rate that banks use to set interest rates for many financial products. When the Federal Reserve adjusts its benchmark rate, banks often respond by adjusting the prime rate as well. This change then flows through to credit cards, adjustable-rate loans, and lines of credit. If you are managing debt or planning to borrow money, knowing how the Fed Prime Rate works can give you a clear advantage.

What Is the Fed Prime Rate and How Is It Set

The Fed Prime Rate is the interest rate that commercial banks charge their most creditworthy customers. It is closely tied to the federal funds rate, which is set by the Federal Reserve. When the Fed raises or lowers the federal funds rate, banks usually adjust the prime rate shortly after. This creates a ripple effect across the financial system, influencing borrowing costs for consumers and businesses alike.

Although the Federal Reserve does not directly set the prime rate, it strongly influences it through its monetary policy decisions. Banks typically add a margin on top of the federal funds rate to determine the prime rate. Because of this connection, the Fed Prime Rate often moves in the same direction as the Fed’s benchmark rate. This relationship is why financial experts closely watch Federal Reserve announcements.

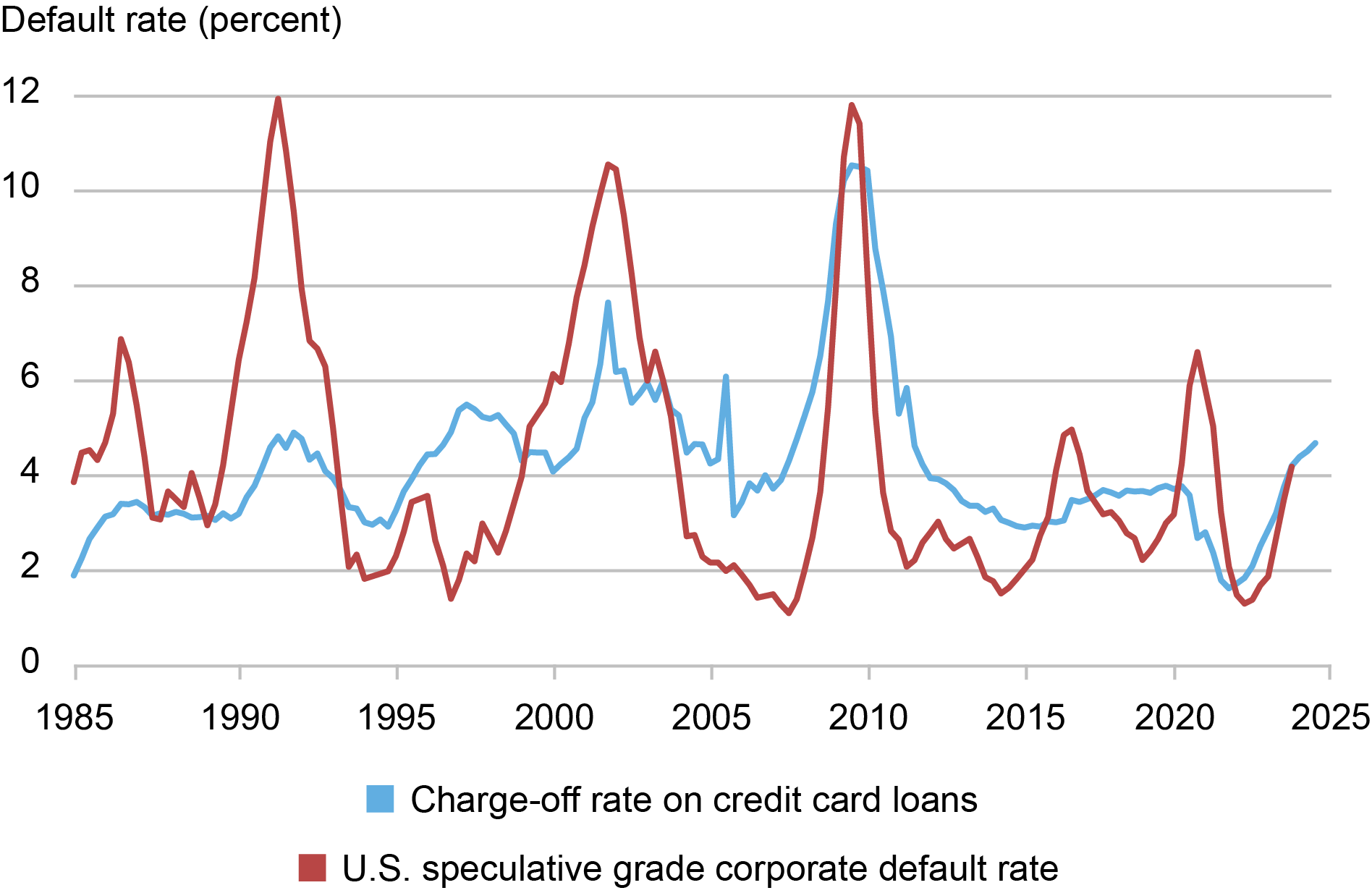

How the Fed Prime Rate Affects Credit Cards

Credit cards are one of the most common financial products linked to the Fed Prime Rate. Most credit card interest rates are variable, meaning they can change over time. These rates are often calculated by adding a fixed margin to the prime rate. When the Fed Prime Rate increases, credit card interest rates usually rise as well, making it more expensive to carry a balance.

For consumers, this means that even a small increase in the prime rate can lead to higher monthly payments. If you have a large credit card balance, a rate hike can significantly increase the total amount of interest you pay over time. On the other hand, when the Fed Prime Rate goes down, it can reduce your interest costs and make it easier to pay off debt. This is why staying informed about rate changes is so important.

The Impact on Personal Loans and Lines of Credit

The Fed Prime Rate also affects personal loans, home equity lines of credit, and other variable-rate borrowing options. Many of these financial products use the prime rate as a starting point to determine interest rates. When the prime rate rises, borrowers with variable-rate loans may see their monthly payments increase, sometimes without much warning.

This can create challenges for people who are already managing tight budgets. Higher interest rates mean more money goes toward interest instead of paying down the principal balance. However, when the Fed Prime Rate falls, borrowers may benefit from lower payments and reduced overall borrowing costs. Understanding this cycle can help you decide when to borrow and when to focus on paying down debt.

Why Lenders Rely on the Fed Prime Rate

Lenders use the Fed Prime Rate because it provides a reliable benchmark for setting interest rates. It reflects the overall cost of borrowing in the economy and helps banks manage risk. By using the prime rate as a base, lenders can adjust their rates quickly in response to changes in the market.

This system also allows lenders to offer competitive rates while still protecting their profit margins. For example, a lender might offer a loan at the prime rate plus a certain percentage, depending on the borrower’s credit profile. This approach makes it easier for banks to price loans consistently and fairly across different customers.

The Connection Between the Fed Prime Rate and the Economy

The Fed Prime Rate is closely linked to the health of the economy. When the economy is growing too quickly and inflation is rising, the Federal Reserve may increase interest rates to slow things down. This often leads to a higher prime rate, which makes borrowing more expensive and encourages people to spend less.

On the other hand, during economic slowdowns, the Fed may lower rates to encourage borrowing and spending. This can lead to a lower prime rate, making credit more affordable for consumers and businesses. These changes are part of the Fed’s strategy to maintain stable prices and support economic growth. For borrowers, this means that the cost of credit can change depending on broader economic conditions.

Smart Strategies for Borrowers in a Changing Rate Environment

Understanding the Fed Prime Rate can help you make better financial decisions, especially when rates are changing. One smart strategy is to pay attention to Federal Reserve announcements and market trends. This can give you an idea of where interest rates might be heading and help you plan accordingly.

Another important step is to manage your debt wisely. If you expect rates to rise, it may be a good idea to pay down high-interest balances or consider fixed-rate options. On the other hand, if rates are falling, you might benefit from refinancing or taking advantage of lower borrowing costs. By staying informed and proactive, you can reduce the impact of rate changes on your finances.

Conclusion

The Fed Prime Rate plays a crucial role in shaping the cost of borrowing for credit cards, loans, and other financial products. Even small changes in this rate can have a big impact on your monthly payments and overall financial health. By understanding how the prime rate works and how it connects to the Federal Reserve’s policies, you can make more informed decisions about borrowing and managing debt.

In today’s fast-changing financial environment, knowledge is one of your strongest tools. Keeping an eye on the Fed Prime Rate and understanding its effects can help you stay ahead of rising costs and take advantage of opportunities when rates fall. Whether you are using credit cards or planning a major loan, being aware of how this key rate influences your finances can lead to smarter, more confident financial choices.